Effects of the ACA on Health Care Coverage for Adults With Substance Use Disorders

Abstract

Objective:

The authors assessed changes in health care coverage in nationally representative samples of low- and middle-income adults with and without substance use disorders following the 2014 Affordable Care Act marketplace launch and Medicaid expansion.

Methods:

Data from the 2012–2018 (N=407,985) National Survey on Drug Use and Health identified low- and middle-income nonelderly adults with alcohol, marijuana, cocaine, or heroin use disorders. A sociodemographically adjusted difference-in-differences analysis assessed the trends in Medicaid and individually purchased private insurance between adults with and without substance use disorders.

Results:

Between 2012–2013 and 2015–2016, the percentages without health insurance significantly declined for adults with substance use disorders (from 27.8% to 18.7%) and for those without these disorders (from 22.6% to 14.6%). These trends were related to gains in Medicaid and in individually purchased private insurance but not to gains in employer-based private insurance coverage. Between 2015–2016 and 2017–2018, however, the percentages without health insurance among adults with substance use disorders (18.7% to 18.4%) and without these disorders (14.7% to 14.7%) was little changed.

Conclusions:

With insurance gains having stalled and the downturn of the U.S. economy, there is renewed urgency to extend health care coverage to middle- and low-income adults with substance use disorders that meets their substance use and general health needs.

HIGHLIGHTS

•

Among U.S. low- and middle-income adults with substance use disorders, the percentages that were uninsured declined from 27.8% (2012–2013) to 18.7% (2015–16) and then remained nearly constant at 18.4% (2017–2018).

•

For adults with substance use disorders, large gains in Medicaid coverage (6.3% to 13.6%) and smaller gains in individually purchased private insurance (5.2% to 7.6%) contributed to a decrease from 2012–2013 to 2015–2016 in the percentage who were uninsured.

•

Gains in insurance coverage have stalled for low- and middle-income adults with substance use disorders, underlining the importance of implementing policies to extend coverage to this vulnerable group.

The benefits of health insurance have been demonstrated through several high-quality studies (1). In a randomized controlled trial, Medicaid recipients experienced significant gains in financial security, improved health-related quality of life, and lower rates of depression, compared with those in a waitlist control group (2). There is also strong evidence that health care coverage improves the likelihood of having a usual source of care (3), accessing preventive services (4), and receiving routine primary care (5) and reduces the risks of premature mortality (4). Because adults with substance use disorders often lack health insurance (6, 7), increasing their health coverage is an important public health goal, even apart from any potential effects on access to substance use services (8, 9).

The Medicaid expansion and health insurance marketplace exchange provisions of the Affordable Care Act (ACA) have the potential to increase insurance coverage for low- and middle-income adults with substance use disorders. Medicaid expansion, which extends Medicaid eligibility to residents of participating states with household incomes up to 138% of the federal poverty level (FPL), contributed to early coverage gains (2012–2013 to 2014–2015) for low-income adults with substance use disorders (10). The health insurance marketplaces offer subsidized health insurance to individuals with incomes between one and four times the FPL. These tax credit subsidies could help low- and middle-income adults with substance use disorders afford coverage. Yet individuals with substance use disorders may have difficulties accessing and navigating marketplace exchanges (11). Although marketplaces accounted for approximately 40% of ACA-related general population coverage gains in 2014 and 2015 (12), it is not known to what extent people with substance use disorders received insurance through marketplaces. Despite a requirement that insurance plans sold through marketplaces offer substance use disorder benefits at parity with medical and surgical benefits, coverage differentials may make these plans less attractive to people with substance use disorders (13).

Following the transition to the Trump administration in January 2017, the new administration issued an executive order seeking to reduce the “economic burden” of the ACA. Shortly after the order, advertising for federally supported marketplaces was reduced, and outreach and consumer assistance for the 2017 marketplace enrollment period declined (14). This was followed by reductions in federal funding for enrollment advertising for the 2018 enrollment period, a decrease in navigator support, and cancelation of $10 billion in payments to insurers for cost-sharing reductions to reimburse low-income marketplace consumers (15). Overall, approximately 12.7 million people were enrolled in health insurance coverage through marketplaces in 2016, 12.2 million in 2017, and 11.8 million in 2018 (16).

Little is known about the effects of this change in policy direction on coverage of low- and middle-income adults with and without substance use disorders. To address this knowledge gap, we compared trends in coverage among adults with and without substance use disorders who reported family income levels that would make them eligible for marketplace premium tax credits. We examined changes in coverage from before the 2014 marketplace launch and Medicaid expansion (2012–2013) to the last 2 years of the Obama administration (2015–2016) and first 2 years of the Trump administration (2017–2018).

Methods

Data Source

The National Survey on Drug Use and Health (NSDUH) is a cross-sectional annual U.S. population survey sponsored by Substance Abuse and Mental Health Services Administration. NSDUH yields national- and state-level representative estimates of substance use disorders for the civilian noninstitutionalized population. Individuals without a household address, active duty military personnel, and institutional residents are excluded from the sampling frame. The NSDUH data collection protocol was approved by the institutional review board at RTI International. The annual mean weighted overall response rate of the 2012–2018 NSDUH surveys was 62.9% (range, 48.8% to 66.8%; total N=407,985) (17).

Background Characteristics

Using DSM-IV criteria, NSDUH yields estimates of past-year dependence on or abuse of alcohol, marijuana, cocaine, and heroin. The survey also collects information on respondent age, sex, race-ethnicity, family income, state of residence, and education level.

Health Insurance

Health insurance status at the time of the survey interview was the outcome. We partitioned insurance status into hierarchical groups of private insurance, Medicaid, other public insurance (Medicare, CHAMPUS, Department of Veterans Affairs, Tricare, or military health), and no insurance. Respondents with private insurance were partitioned into employer-based coverage, defined as coverage “provided through work, such as through an employer, union, or professional association,” and individually purchased private coverage, defined as private coverage not provided through work. We considered individually purchased private coverage as a proxy for marketplace-purchased plans.

Medicaid Expansion State Residence

States were partitioned by Medicaid expansion implementation status (18). By the end of 2014, 26 states and the District of Columbia had expanded Medicaid and are referred to as expansion states. The remaining 24 states are referred to as nonexpansion states. (A table in an online supplement to this article lists the expansion and nonexpansion states.)

Statistical Analysis

We examined whether health insurance coverage trends differed among adults with and without substance use disorders. Because we focused on potential effects of marketplace tax credits on individually purchased plans, we limited the analysis to adults ages 18–64 years with family incomes of 100%−400% of FPL that enabled them to receive tax credits. Baseline sociodemographic characteristics were first compared among adults with and without past-year substance use disorders.

To distinguish coverage trends under policies of the Obama and Trump administrations, we considered coverage from before ACA implementation (2012–2013) to the last 2 years of the Obama administration (2015–2016) and the first 2 years of the Trump administration (2017–2018), leaving out the year of policy implementation (2014). We used a difference-in-differences design (19) to assess differences in secular trends in insurance coverage between populations with and without past-year substance use disorders. Multivariable logistic regression analyses estimated changes in coverage prevalence and included the effects of categorical survey years, a substance use disorder dummy variable, an interaction term for year × substance use disorder, and covariates age, sex, race-ethnicity, region, and education. Some models compared 2012–2013 with 2015–2016, and others compared 2015–2016 with 2017–2018, providing flexibility for the covariate distribution to be controlled separately in the two periods. Because covariate distributions varied between models, estimated insurance percentages for 2015–2016 may vary between models. Adjusted difference estimates in coverage prevalence (back-transformed from marginal log-odds) (20) tested change in coverage over time among adults with and without substance use disorders. The interaction contrast on the predicted prevalence scale from the model provided the difference-in-differences test of whether changes over time differed between adults with and without substance use disorders. Percentages, differences, and difference-in-differences estimates were adjusted for age, sex, race-ethnicity, region, and education level.

Because the value of marketplace premium subsidies declines with increasing income from 100% to 400% of FPL, lower-income individuals have stronger financial incentives to purchase marketplace plans (21). To assess this effect, analyses were stratified by poverty level (100%−200% versus 201%−400%). Because lower-income adults in Medicaid nonexpansion states, compared with expansion states, have fewer affordable coverage options, we compared coverage trends among expansion and nonexpansion state residents with and without substance use disorders. SAS, version 9, callable SUDAAN using PROC MULTILOG was used to account for NSDUH’s complex sample design and sample weights.

Results

Background Characteristics

Among adults whose incomes were 100% to 400% of the FPL, background characteristics were compared between those with and without past-year substance use disorders. Compared with those without substance use disorders, those with these disorders were more likely in each of the three study periods to be male, ages 18 to 24 or 35 to 44 years, and White non-Hispanic; to have lower family incomes; and not to have graduated from college (Table 1). Of those in the substance use disorder group, the largest proportions met criteria for alcohol use disorder.

| 2012–2013 | 2015–2016 | 2017–2018 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Past-year substance use disorder | Past-year substance use disorder | Past-year substance use disorder | |||||||||||||

| Yes | No | Yes | No | Yes | No | ||||||||||

| Characteristic | % | SE | % | SE | p | % | SE | % | SE | p | % | SE | % | SE | p |

| Age | <.001 | <.001 | <.001 | ||||||||||||

| 18–24 | 30.5 | .9 | 15.5 | .2 | 26.4 | .7 | 15.2 | .2 | 26.8 | .8 | 15.4 | .2 | |||

| 25–34 | 30.8 | 1.1 | 23.1 | .4 | 33.1 | .9 | 23.5 | .3 | 33.1 | 1.0 | 24.0 | .3 | |||

| 35–44 | 18.0 | 1.0 | 22.7 | .3 | 17.2 | .8 | 20.4 | .3 | 18.2 | .8 | 21.0 | .3 | |||

| 45–64 | 20.8 | 1.2 | 38.7 | .5 | 23.4 | 1.1 | 40.9 | .4 | 21.8 | 1.1 | 39.6 | .4 | |||

| Sex | <.001 | <.001 | <.001 | ||||||||||||

| Male | 67.4 | 1.1 | 47.3 | .4 | 65.7 | .9 | 47.5 | .3 | 66.7 | .9 | 47.8 | .3 | |||

| Female | 32.6 | 1.1 | 52.7 | .4 | 34.3 | .9 | 52.5 | .3 | 33.3 | .9 | 52.2 | .3 | |||

| Race-ethnicity | .002 | <.001 | <.001 | ||||||||||||

| White, non-Hispanic | 61.6 | 1.2 | 59.5 | .6 | 62.6 | 1.0 | 59.0 | .5 | 61.0 | 1.0 | 55.9 | .5 | |||

| Black, non-Hispanic | 13.3 | .8 | 13.1 | .4 | 12.1 | .7 | 13.5 | .3 | 13.1 | .7 | 14.1 | .3 | |||

| Hispanic | 19.2 | 1.0 | 19.3 | .4 | 19.9 | .9 | 20.0 | .4 | 19.2 | .9 | 21.7 | .4 | |||

| Other | 5.9 | .5 | 8.1 | .3 | 5.5 | .4 | 7.5 | .2 | 6.6 | .5 | 8.3 | .3 | |||

| Education | <.001 | .017 | .042 | ||||||||||||

| Less than high school graduate | 16.1 | .8 | 13.5 | .3 | 14.2 | .8 | 13.3 | .3 | 12.6 | .7 | 13.3 | .3 | |||

| High school graduate | 32.6 | 1.1 | 34.0 | .4 | 29.2 | .9 | 29.2 | .3 | 30.4 | 1.0 | 28.9 | .3 | |||

| Some college | 32.8 | 1.1 | 30.3 | .4 | 37.7 | .9 | 36.1 | .3 | 37.7 | 1.0 | 36.3 | .3 | |||

| College graduate | 18.5 | .9 | 22.2 | .4 | 18.9 | .8 | 21.4 | .3 | 19.4 | .8 | 21.4 | .3 | |||

| Income (M $) | 43,223 | 509 | 47,853 | 232 | <.001 | 46,231 | 447 | 49,550 | 169 | <.001 | 45,053 | 466 | 49,603 | 184 | <.001 |

| Past-year substance use disorder | |||||||||||||||

| Alcohol | 84.6 | .9 | — | 83.6 | .7 | — | 79.8 | .8 | — | ||||||

| Marijuana | 19.1 | .9 | — | 20.8 | .8 | — | 23.8 | .9 | — | ||||||

| Cocaine | 5.0 | .5 | — | 5.4 | .5 | — | 6.2 | .5 | — | ||||||

| Heroin | 2.6 | .3 | — | 3.9 | .4 | — | 3.7 | .4 | — | ||||||

a

Data from the National Survey on Drug Use and Health. Income eligible was defined as between 100% and 400% of the federal poverty level. The Substance Abuse and Mental Health Services Administration, which conducts the survey, requires that all descriptions of overall sample sizes based on the public-use data files and are rounded to the nearest 100 to minimize potential disclosure risk.

Lack of Insurance

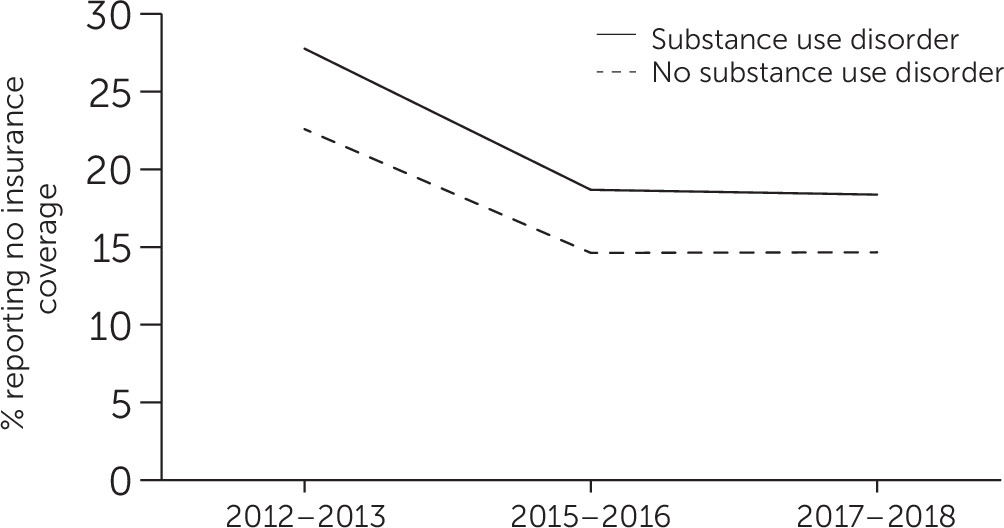

Trends in uninsured rates were compared before (2012–2013) and after (2015–2016) the ACA policies were implemented and between 2015–2016 and 2017–2018 (Figure 1). Between 2012–2013 and 2015–2016, the percentage of adults with substance use disorders who were uninsured declined from 27.8% to 18.7% (difference=−9.1%, 95% confidence interval [CI]=−11.6 to –6.6), and the percentage without substance use disorders who were uninsured declined from 22.6% to 14.6% (difference=−8.0%, 95% CI=−8.9 to –7.1). The difference-in-differences estimate was not significant. Between 2015–2016 and 2017–2018, the percentage of each group that was uninsured was little changed.

FIGURE 1. Trends in no insurance coverage among low- and middle-income adults with and without selected substance use disorders, 2012–2018a

aData from the National Survey on Drug Use and Health for adults with alcohol, marijuana, cocaine, or heroin use disorders. Between 2012–2013 and 2015–2016, the estimated changes in the percentage without insurance were –9.1% (95% confidence interval [CI]=–11.6, –6.6) for adults with substance use disorders and –8.0% (95% CI=−8.9, –7.1) for those without these disorders. Between 2015–2016 and 2017–2018, the estimated changes were –0.3% (95% CI=−2.5, 1.8) for adults with substance use disorders and 0% (95% CI=−0.7, 0.7) for those without these disorders. Differences were adjusted for age, sex, race-ethnicity, region, and education. For ease of presentation, 2015–2016 data are presented as means of modeled estimates from 2012–2013/2015–2016 and 2015–2016/2017–2018 models.

Individually Purchased and Employer-Purchased Private Insurance

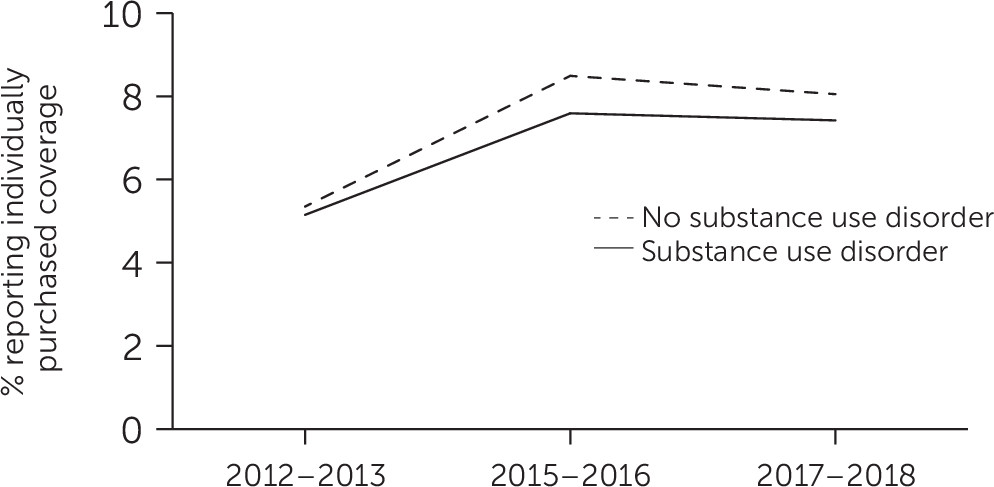

From 2012–2013 to 2015–2016, individually purchased private insurance coverage for adults with substance use disorders significantly increased from 5.2% to 7.6% (difference=2.4 percentage points, 95% CI=0.8 to 4.1), and for those without substance use disorders it increased from 5.4% to 8.5% (difference=3.1 percentage points, 95% CI=2.6 to 3.7) (difference in differences=−0.7%, 95% CI=−2.4 to 1.0) (Figure 2). Between 2015–2016 and 2017–2018, there was not a significant change in individually purchased private insurance for adults with or without substance use disorders. Between 2012–2013 and 2015–2016 and between 2015–2016 and 2017–2018, the proportions of adults with and without substance use disorders who had employer-based private insurance were little changed (see figure in online supplement ).

FIGURE 2. Trends in private individually purchased insurance among low- and middle-income adults with and without selected substance use disorders, 2012–2018a

aData from the National Survey on Drug Use and Health for adults with alcohol, marijuana, cocaine, or heroin use disorders. Between 2012–2013 and 2015–2016, the estimated changes in private individually purchased insurance were 2.4% (95% confidence interval [CI]=0.8, 4.1) for adults with substance use disorders and 3.1% (95% CI=2.6, 3.7) for those without these disorders. Between 2015–2016 and 2017–2018, the estimated changes were –0.5% (95% CI=−2.1, 1.3) for adults with substance use disorders and –0.4% (95% CI=−1.0%, 0.2%) for those without these disorders. Differences were adjusted for age, sex, race-ethnicity, region, and education. For ease of presentation, 2015–2016 data are presented as means of modeled estimates from 2012–2013/2015–2016 and 2015–2016/2017–2018 models.

Medicaid Coverage and Other Public Insurance

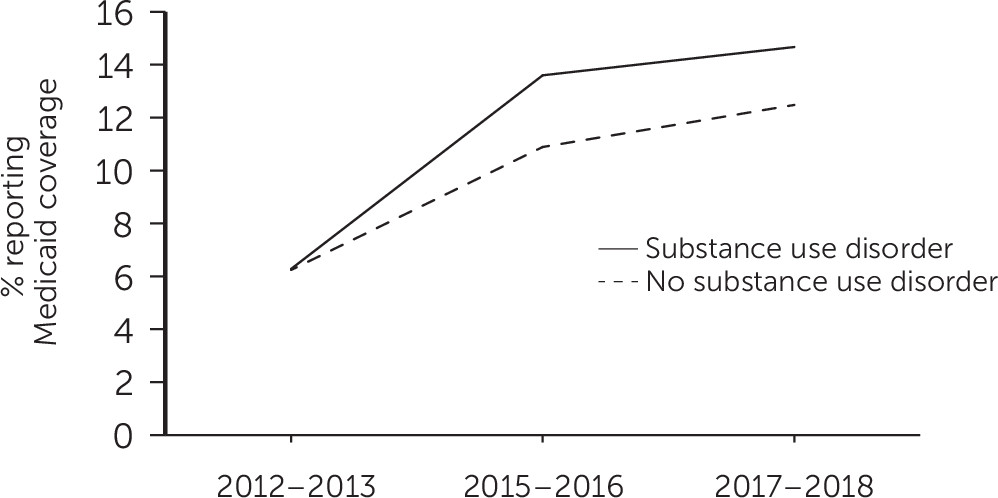

Medicaid coverage increased between 2012–2013 and 2015–2016 significantly more for adults with substance use disorders (6.3% to 13.6%, difference=7.3 percentage points, 95% CI=5.7 to 8.9), compared with adults without substance use disorders (6.2% to 10.9%, difference=4.6 percentage points, 95% CI=4.1 to 5.2) (difference in differences=2.7%, 95% CI=1.0 to 4.4) (Figure 3). During the following period, there was a small and statistically nonsignificant increase in Medicaid coverage for adults with substance use disorders (13.4% to 14.7%, difference=1.3 percentage points, 95% CI=−0.6 to 3.2) and an increase for those without substance use disorders (10.8% to 12.5%, difference=1.7 percentage points, 95% CI=1.1 to 2.3) (difference in differences=−0.4%, 95% CI=–2.4 to 1.6).

FIGURE 3. Trends in Medicaid coverage among low- and middle-income adults with and without selected substance use disorders, 2012–2018a

aData from the National Survey on Drug Use and Health for adults with alcohol, marijuana, cocaine, or heroin use disorders. Between 2012–2013 and 2015–2016, the estimated changes in Medicaid coverage were 7.3% (95% confidence interval [CI]=5.7, 8.9) for adults with substance use disorders and 4.6% (95% CI=4.1, 5.2) for those without these disorders (difference, 2.7%, 95% CI=1.0, 4.4). Between 2015–2016 and 2017–2018, the estimated changes were 1.3% (95% CI=−0.6, 3.2) for adults with substance use disorders and 1.7% (95% CI=1.1, 2.3) for those without these disorders. Differences were adjusted for age, sex, race-ethnicity, region, and education. For ease of presentation, 2015–2016 data are presented as means of modeled estimates from 2012–2013/2015–2016 and 2015–2016/2017–2018 models.

Between 2012–2013 and 2015–2016, there was little change in other public insurance among adults with substance use disorders (9.8% to 9.6%) and an increase among those without substance use disorders (8.6% to 9.4%, difference=0.9 percentage points, 95% CI=0.2 to 1.5). From 2015–2016 to 2017–2018, however, there was no change in other public insurance among adults with and without substance use disorders (see figure in online supplement ).

Family Income and Individually Purchased Private Insurance

Among adults with substance use disorders, gains in individually purchased private insurance between 2012–13 and 2015–16 were roughly similar in the two income groups: 5.5% to 8.1% in the group at 100%−200% of FPL (difference=2.6 percentage points, 95% CI=−0.1 to 5.4) and 5.0% to 7.3% in the group at 201%−400% of FPL (difference=2.3 percentage points, 95% CI=0.4 to 4.3) (see figure in online supplement ). Among those without substance use disorders, the corresponding gain was greater in the lower-income group (5.5% to 9.9%, difference=4.4 percentage points, 95% CI=3.4 to 5.4), compared with the higher-income group (5.3% to 7.7%, difference=2.4 percentage points, 95% CI=1.7 to 3.2). Between 2015–2016 and 2017–2018, little change was noted in the percentages with individually purchased private insurance in either income group of adults with and without substance use disorders.

State Residence and Health Insurance

Among residents of Medicaid expansion states, the increase in Medicaid enrollment between 2012–2013 and 2015–2016 was larger for people with substance use disorders than for those without substance use disorders (see figure in online supplement ). Less change was noted in Medicaid enrollment in nonexpansion states during this period. Among adults with substance use disorders, the percentage with individually purchased private insurance significantly increased from 2012–2013 to 2015–2016 in nonexpansion states but not in expansion states (see figure in online supplement ). Between 2015–2016 and 2017–2018, little change occurred in the percentage of adults with substance use disorders with individually purchased private insurance in either expansion or nonexpansion states. Similar patterns were observed among those without substance use disorders.

Discussion

Consistent with prior research (10), a decline was noted in the percentage of low- and middle-income adults who were uninsured during the first 2 years following implementation of Medicaid expansion and marketplace exchanges. Following the change in administrations between 2015–2016 and 2017–2018, however, the proportion that was uninsured remained unchanged. This new finding was also observed among low- and middle-income adults without substance use disorders. Opposition to the ACA under the Trump administration may have contributed to ending the decline in the percentages of these two groups of low- and middle-income adults without health insurance. During 2017–2018, there was a shift in federal health care policy away from the ACA reflected in public statements (22) and actions, including a reduction in advertising marketplace enrollment, shortening of the enrollment period (14), and cancelation of reimbursement payments to insurers for low-income marketplace withholding that may have slowed enrollment of lower-income people (23).

Between 2012–2013 and 2015–2016, trends in insurance coverage were consistent with Medicaid expansion and health insurance marketplace policies. Growth occurred in Medicaid coverage and individually purchased private coverage among low- and middle-income adults with and without substance use disorders. Meanwhile, coverage changed less in other public insurance programs and in employee-sponsored private insurance plans that were not a focus of these two ACA provisions.

Under the marketplace provision, individuals with family incomes of 100%−400% of the FPL are eligible for premium tax credits to reduce premium payments. Because the subsidies are progressive (24), the increase in individually purchased private plans was expected to be greater among adults in the lower group, compared with the upper group, of this income range. Although evidence of such an effect was noted among adults without substance use disorders, gains in individually purchased private coverage were similar for the two income groups with substance use disorders (see figure in online supplement ). Lower-income adults with substance use disorders may have had greater difficulties in accessing benefits available to them through the marketplace exchanges, compared with their counterparts without substance use disorders. Detailed prospective research could help identify which outreach strategies are most helpful for which populations in achieving marketplace enrollment (25).

It is not known why adults with substance use disorders were relatively less likely than those without substance use disorders to take advantage of marketplace subsidies. Some possibilities include more challenging life circumstances, competing priorities for basic daily needs (26), or more extensive reliance on navigators for enrollment assistance. During the Trump administration, federal funding for ACA navigators was reduced by 43% between 2016 and 2017 and by 72% between 2017 and 2018 (27).

The increase in Medicaid coverage following expansion, by contrast, was proportionately greater for adults with substance use disorders, compared with those without substance use disorders. Lower average incomes of adults with substance use disorders may have resulted in a larger proportion being eligible for Medicaid under ACA expansion (28). Medicaid coverage plays an important role in the availability of substance use services (29) and general medical services (30) for individuals with substance use disorders. Expansion by states of Medicaid eligibility has been associated with slower growth in drug overdose (31) and in deaths related to substance use disorders (32). Although Medicaid coverage gains were concentrated in expansion states, a larger share of adults with substance use disorders, compared with those without these disorders, remained uninsured throughout the study period.

Compared with the gains seen under Medicaid expansion, marketplace exchanges have been associated with smaller gains in coverage for adults with incomes of 100%−138% of the poverty level (33). A similar pattern was observed even among a broader income group with substance use disorders, many of whom were not income eligible for Medicaid. Higher premiums for marketplace plans, compared with Medicaid coverage, or greater difficulties navigating marketplace enrollment, compared with Medicaid enrollment, may have contributed to their having a relatively smaller increase in individually purchased private plans, compared with Medicaid.

The findings suggest that adults with substance use disorders increased enrollment in Medicaid and individually purchased private insurance plans in the years immediately following ACA policy implementation (implemented in 2014). However, because the findings capture coverage at the time of the survey, the results likely understate percentages of adults who were uninsured at some point during each year. In a recent study, nearly one-quarter of marketplace beneficiaries disenrolled before the end of the year (34). From the insurers’ perspective, adults with substance use disorders are among the least desirable to insure because their health care expenditures often exceed their premiums (35), making them a group vulnerable to disenrollment. In an analysis of Medicaid enrollees, disenrollment was greater among adults with substance use problems, compared with those without these problems (36). Despite coverage gains, expanding coverage for lower-income adults with substance use disorders, such as through incentivizing insurers to participate in marketplaces and adjusting risk through more generous premium tax credits (37), remains a key public health care policy challenge. In evaluating these findings, it is important to bear in mind that most of the adults with substance use disorders had alcohol use disorder. Compared with adults with drug use disorders, those with alcohol use disorders may have faced fewer barriers to health insurance following ACA implementation.

This analysis had some limitations. First, a change in NSDUH survey design prevented an examination of trends in coverage of adults with prescription stimulant, sedative, or opioid use disorders other than heroin use disorder. Second, NSDUH did not sample homeless individuals not living in shelters, active duty military personnel, or persons residing in institutions. Third, NSDUH did not directly assess whether insurance coverage was purchased from marketplaces. Instead, it was assumed that private insurance not purchased through an employer, union, or professional association was individually purchased on a marketplace. In addition, no effort was made to distinguish federally facilitated from state-based marketplaces. Fourth, the difference-in-differences models assume that without Medicaid expansion, insurance trends in expansion and nonexpansion states would have been constant over time. However, ACA provisions other than Medicaid expansion and marketplaces, such as the employer mandate (38) and dependent coverage provision (39), or other factors that were not controlled for in the models may have contributed to differential changes in coverage in expansion and nonexpansion states. Finally, the analysis did not assess the effects of coverage on substance use treatment or other health care use. Some prior research suggests that increases in coverage alone may not be sufficient to increase substance use treatment (10, 40). Beyond health insurance, several other factors, such as transportation, service availability, stigma, and perceived effectiveness of treatment, may influence access to needed behavioral health services (41). A lack of local providers may help explain why gains in coverage may not be sufficient to increase treatment (42).

Conclusions

In the first 2 years following implementation of the 2014 ACA marketplace and Medicaid expansion provisions (2015–2016), there was a decline in the percentage of low- and middle-income adults with common substance use disorders who were uninsured. The decline halted after the change of administrations in 2017. Although the percentage who were uninsured remained higher among low- and middle-income adults with substance use disorders, compared with those without these disorders, lower percentages of both those with and without substance use disorders were uninsured in 2017–2018, compared with before implementation of the ACA provisions in 2014. During the pandemic-induced economic downturn, particularly in light of the association between financial strain and serious substance use problems (43), it will be critically important to implement policies that extend health care coverage to uninsured low- and middle-income individuals with substance use disorders.

Supplementary Material

File (appi.ps.202000377.ds001.pdf)

- View/Download

- 97.86 KB

References

1.

Sommers BD, Gawande AA, Baicker K: Health insurance coverage and health: what the recent evidence tells us. N Engl J Med 2017; 377:586–593

2.

Baicker K, Taubman SL, Allen HL, et al: The Oregon experiment: effects of Medicaid on clinical outcomes. N Engl J Med 2013; 368:1713–1722

3.

Shartzer A, Long SK, Anderson N: Access to care and affordability have improved following Affordable Care Act implementation; problems remain. Health Aff 2016; 35:161–168

4.

Sommers BD, Long SK, Baicker K: Changes in mortality after Massachusetts health care reform: a quasi-experimental study. Ann Intern Med 2014; 160:585–593

5.

Sommers BD, Gunja MZ, Finegold K, et al: Changes in self-reported insurance coverage, access to care, and health under the Affordable Care Act. JAMA 2015; 314:366–374

6.

Saloner B, Bandara S, Bachhuber M, et al: Insurance coverage and treatment use under the Affordable Care Act among adults with mental and substance use disorders. Psychiatr Serv 2017; 68:542–548

7.

Wang N, Xie X: The impact of race, income, drug abuse and dependence on health insurance coverage among US adults. Eur J Health Econ 2017; 18:537–546

8.

Ali MM, Teich JL, Mutter R: Reasons for not seeking substance use disorder treatment: variations by health insurance coverage. J Behav Health Serv Res 2017; 44:63–74

9.

2015 National Survey on Drug Use and Health: Detailed Tables. Rockville, MD, Substance Abuse and Mental Health Services Administration, 2016

10.

Olfson M, Wall M, Barry CL, et al: Impact of Medicaid expansion on coverage and treatment of low-income adults with substance use disorders. Health Aff 2018; 37:1208–1215

11.

McCabe HA, Wahler EA: The Affordable Care Act, substance use disorders, and low-income clients: implications for social work. Soc Work 2016; 61:227–233

12.

Frean M, Gruber J, Sommers BD: Premium subsidies, the mandate, and Medicaid expansion: coverage effects of the Affordable Care Act. J Health Econ 2017; 53:72–86

13.

Berry KN, Huskamp HA, Goldman HH, et al: A tale of two states: do consumers see mental health insurance parity when shopping on state exchanges? Psychiatr Serv 2015; 66:565–567

14.

Anderson D, Shafer P: The Trump effect: postinauguration changes in Marketplace enrollment. J Health Polit Policy Law 2019; 44:715–736

15.

Jost TS: ACA open enrollment starts amidst tumult. Health Aff 2017; 36:2044–2045

16.

Health Insurance Exchanges 2018 Open Enrollment Period Final Report. Baltimore, Centers for Medicare and Medicaid Services, April 03, 2018. https://www.cms.gov/newsroom/fact-sheets/health-insurance-exchanges-2018-open-enrollment-period-final-report

17.

National Survey on Drug Use and Health. Rockville, MD, Substance Abuse and Mental Health Services Administration. https://nsduhweb.rti.org/respweb/homepage.cfm. Accessed May 13, 2020

18.

Status of State Action on the Medicaid Expansion Decision. Menlo Park, CA, Kaiser Family Foundation, Kaiser Commission on Medicaid and the Uninsured, 2017. https://www.kff.org/health-reform/state-indicator/state-activity-around-expanding-medicaid-under-the-affordable-care-act/

19.

Imbens GW, Wooldridge JM: Recent developments in the econometrics of program evaluation. J Econ Lit 2009; 47:5–86

20.

Bieler GS, Brown GG, Williams RL, et al: Estimating model-adjusted risks, risk differences, and risk ratios from complex survey data. Am J Epidemiol 2010; 171:618–623

21.

Goldman AL, McCormick D, Haas JS, et al: Effects of the ACA’s health insurance marketplaces on the previously uninsured: a quasi-experimental analysis. Health Aff 2018; 37:591–599

22.

Haberman M, Pear R: Trump tells Congress to repeal and replace health care law “very quickly.” NY Times, Jan 10, 2017

23.

Drake C, Anderson DM: Terminating cost-sharing reduction subsidy payments: the impact of Marketplace zero-dollar premium plans on enrollment. Health Aff 2020; 39:41–49

24.

Eligibility for the Premium Tax Credit. Washington, DC, Internal Revenue Service, 2020. https://www.irs.gov/affordable-care-act/individuals-and-families/eligibility-for-the-premium-tax-credit. Accessed April 10, 2020

25.

Giovannelli J, Curran E: Factors affecting health insurance enrollment through the state marketplaces: observations on the ACA’s third open enrollment period. Issue Brief Commonw Fund) 2016; 19:1–12

26.

Stopka TJ, Hutcheson M, Donahue A: Access to healthcare insurance and healthcare services among syringe exchange program clients in Massachusetts: qualitative findings from health navigators with the iDU (“I do”) Care Collaborative. Harm Reduct J 2017; 14:26

27.

Pollitz K, Tolbert J, Diaz M: Data Note: Limited Navigator Funding for Federal Marketplace States. Menlo Park, CA, Kaiser Family Foundation, Nov 13, 2019. https://www.kff.org/private-insurance/issue-brief/data-note-further-reductions-in-navigator-funding-for-federal-marketplace-states/. Accessed July 5, 2020

28.

Zur J, Musumeci M, Garfield R: Medicaid’s Role in Financing Behavioral Health Services for Low-Income Individuals. Menlo Park, CA, Kaiser Family Foundation, June 2017. http://files.kff.org/attachment/Issue-Brief-Medicaids-Role-in-Financing-Behavioral-Health-Services-for-Low-Income-Individuals. Accessed July 6, 2020

29.

Abraham AJ, Rieckmann T, Andrews CM, et al: Health insurance enrollment and availability of medications for substance use disorders. Psychiatr Serv 2017; 68:41–47

30.

Lillie-Blanton M, Stone VE, Snow Jones A, et al: Association of race, substance abuse, and health insurance coverage with use of highly active antiretroviral therapy among HIV-infected women, 2005. Am J Public Health 2010; 100:1493–1499

31.

Venkataramani AS, Chatterjee P: Early Medicaid expansions and drug overdose mortality in the USA: a quasi-experimental analysis. J Gen Intern Med 2019; 34:23–25

32.

Snider JT, Duncan ME, Gore MR, et al: Association between state Medicaid eligibility thresholds and deaths due to substance use disorders. JAMA Netw Open 2019; 2:e193056

33.

Blavin F, Karpman M, Kenney GM, et al: Medicaid versus Marketplace coverage for near-poor adults: effects on out-of-pocket spending and coverage. Health Aff 2018; 37:299–307

34.

Gordon SH, Sommers BD, Wilson IB, et al: Risk factors for early disenrollment for Colorado’s Affordable Care Act Marketplace. Med Care 2019; 57:49–53

35.

McGuire TG, Newhouse JP, Normand S-L, et al: Assessing incentives for service-level selection in private health insurance exchanges. J Health Econ 2014; 35:47–63

36.

Wallace NT, McConnell KJ, Gallia CA, et al: Benefit policy and disenrollment of adult Medicaid beneficiaries from the Oregon health plan. J Health Care Poor Underserved 2010; 21:1382–1394

37.

Karpman M, Long SK, Bart L: The Affordable Care Act’s Marketplaces expanded insurance coverage for adults with chronic health conditions. Health Aff 2018; 37:600–606

38.

Glied S, Solis-Roman C: What Will Be the Impact of the Employer Mandate on the US Workforce? Issue Brief, pub 1778. New York, Commonwealth Fund, Oct 2014

39.

Olfson M, Wall M, Barry CL, et al: Effects of the Affordable Care Act on private insurance coverage and treatment of behavioral health conditions in young adults. Am J Public Health 2018; 108:1352–1354

40.

Capoccia VA, Grazier KL, Toal C, et al: Massachusetts’s experience suggests coverage alone is insufficient to increase addiction disorders treatment. Health Aff 2012; 31:1000–1008

41.

Mojtabai R, Olfson M, Sampson NA, et al: Barriers to mental health treatment: results from the National Comorbidity Survey Replication. Psychol Med 2011; 41:1751–1761

42.

Gertner AK, Robertson AG, Jones H, et al: The effect of Medicaid expansion on use of opioid agonist treatment and the role of provider capacity constraints. Health Serv Res 2020; 55:383–392

43.

Venkataramani AS, Bair EF, O’Brien RL, et al: Association between automotive assembly plant closures and opioid overdose mortality in the United States: a difference-in-differences analysis. JAMA Intern Med 2020; 180:254–262

Information & Authors

Information

Published In

History

Received: 25 May 2020

Revision received: 1 September 2020

Accepted: 15 October 2020

Published online: 7 May 2021

Published in print: August 01, 2021

Keywords

Authors

Funding Information

This work is supported by grant R01 DA019606 from the National Institute on Drug Abuse.The authors report no financial relationships with commercial interests.

Metrics & Citations

Metrics

Citations

Export Citations

If you have the appropriate software installed, you can download article citation data to the citation manager of your choice. Simply select your manager software from the list below and click Download.

For more information or tips please see 'Downloading to a citation manager' in the Help menu.

View Options

View options

PDF/EPUB

View PDF/EPUBMedia

Figures

FIGURE 1. Trends in no insurance coverage among low- and middle-income adults with and without selected substance use disorders, 2012–2018a

aData from the National Survey on Drug Use and Health for adults with alcohol, marijuana, cocaine, or heroin use disorders. Between 2012–2013 and 2015–2016, the estimated changes in the percentage without insurance were –9.1% (95% confidence interval [CI]=–11.6, –6.6) for adults with substance use disorders and –8.0% (95% CI=−8.9, –7.1) for those without these disorders. Between 2015–2016 and 2017–2018, the estimated changes were –0.3% (95% CI=−2.5, 1.8) for adults with substance use disorders and 0% (95% CI=−0.7, 0.7) for those without these disorders. Differences were adjusted for age, sex, race-ethnicity, region, and education. For ease of presentation, 2015–2016 data are presented as means of modeled estimates from 2012–2013/2015–2016 and 2015–2016/2017–2018 models.

FIGURE 2. Trends in private individually purchased insurance among low- and middle-income adults with and without selected substance use disorders, 2012–2018a

aData from the National Survey on Drug Use and Health for adults with alcohol, marijuana, cocaine, or heroin use disorders. Between 2012–2013 and 2015–2016, the estimated changes in private individually purchased insurance were 2.4% (95% confidence interval [CI]=0.8, 4.1) for adults with substance use disorders and 3.1% (95% CI=2.6, 3.7) for those without these disorders. Between 2015–2016 and 2017–2018, the estimated changes were –0.5% (95% CI=−2.1, 1.3) for adults with substance use disorders and –0.4% (95% CI=−1.0%, 0.2%) for those without these disorders. Differences were adjusted for age, sex, race-ethnicity, region, and education. For ease of presentation, 2015–2016 data are presented as means of modeled estimates from 2012–2013/2015–2016 and 2015–2016/2017–2018 models.

FIGURE 3. Trends in Medicaid coverage among low- and middle-income adults with and without selected substance use disorders, 2012–2018a

aData from the National Survey on Drug Use and Health for adults with alcohol, marijuana, cocaine, or heroin use disorders. Between 2012–2013 and 2015–2016, the estimated changes in Medicaid coverage were 7.3% (95% confidence interval [CI]=5.7, 8.9) for adults with substance use disorders and 4.6% (95% CI=4.1, 5.2) for those without these disorders (difference, 2.7%, 95% CI=1.0, 4.4). Between 2015–2016 and 2017–2018, the estimated changes were 1.3% (95% CI=−0.6, 3.2) for adults with substance use disorders and 1.7% (95% CI=1.1, 2.3) for those without these disorders. Differences were adjusted for age, sex, race-ethnicity, region, and education. For ease of presentation, 2015–2016 data are presented as means of modeled estimates from 2012–2013/2015–2016 and 2015–2016/2017–2018 models.

Other

Tables

References

References

1.

Sommers BD, Gawande AA, Baicker K: Health insurance coverage and health: what the recent evidence tells us. N Engl J Med 2017; 377:586–593

2.

Baicker K, Taubman SL, Allen HL, et al: The Oregon experiment: effects of Medicaid on clinical outcomes. N Engl J Med 2013; 368:1713–1722

3.

Shartzer A, Long SK, Anderson N: Access to care and affordability have improved following Affordable Care Act implementation; problems remain. Health Aff 2016; 35:161–168

4.

Sommers BD, Long SK, Baicker K: Changes in mortality after Massachusetts health care reform: a quasi-experimental study. Ann Intern Med 2014; 160:585–593

5.

Sommers BD, Gunja MZ, Finegold K, et al: Changes in self-reported insurance coverage, access to care, and health under the Affordable Care Act. JAMA 2015; 314:366–374

6.

Saloner B, Bandara S, Bachhuber M, et al: Insurance coverage and treatment use under the Affordable Care Act among adults with mental and substance use disorders. Psychiatr Serv 2017; 68:542–548

7.

Wang N, Xie X: The impact of race, income, drug abuse and dependence on health insurance coverage among US adults. Eur J Health Econ 2017; 18:537–546

8.

Ali MM, Teich JL, Mutter R: Reasons for not seeking substance use disorder treatment: variations by health insurance coverage. J Behav Health Serv Res 2017; 44:63–74

9.

2015 National Survey on Drug Use and Health: Detailed Tables. Rockville, MD, Substance Abuse and Mental Health Services Administration, 2016

10.

Olfson M, Wall M, Barry CL, et al: Impact of Medicaid expansion on coverage and treatment of low-income adults with substance use disorders. Health Aff 2018; 37:1208–1215

11.

McCabe HA, Wahler EA: The Affordable Care Act, substance use disorders, and low-income clients: implications for social work. Soc Work 2016; 61:227–233

12.

Frean M, Gruber J, Sommers BD: Premium subsidies, the mandate, and Medicaid expansion: coverage effects of the Affordable Care Act. J Health Econ 2017; 53:72–86

13.

Berry KN, Huskamp HA, Goldman HH, et al: A tale of two states: do consumers see mental health insurance parity when shopping on state exchanges? Psychiatr Serv 2015; 66:565–567

14.

Anderson D, Shafer P: The Trump effect: postinauguration changes in Marketplace enrollment. J Health Polit Policy Law 2019; 44:715–736

15.

Jost TS: ACA open enrollment starts amidst tumult. Health Aff 2017; 36:2044–2045

16.

Health Insurance Exchanges 2018 Open Enrollment Period Final Report. Baltimore, Centers for Medicare and Medicaid Services, April 03, 2018. https://www.cms.gov/newsroom/fact-sheets/health-insurance-exchanges-2018-open-enrollment-period-final-report

17.

National Survey on Drug Use and Health. Rockville, MD, Substance Abuse and Mental Health Services Administration. https://nsduhweb.rti.org/respweb/homepage.cfm. Accessed May 13, 2020

18.

Status of State Action on the Medicaid Expansion Decision. Menlo Park, CA, Kaiser Family Foundation, Kaiser Commission on Medicaid and the Uninsured, 2017. https://www.kff.org/health-reform/state-indicator/state-activity-around-expanding-medicaid-under-the-affordable-care-act/

19.

Imbens GW, Wooldridge JM: Recent developments in the econometrics of program evaluation. J Econ Lit 2009; 47:5–86

20.

Bieler GS, Brown GG, Williams RL, et al: Estimating model-adjusted risks, risk differences, and risk ratios from complex survey data. Am J Epidemiol 2010; 171:618–623

21.

Goldman AL, McCormick D, Haas JS, et al: Effects of the ACA’s health insurance marketplaces on the previously uninsured: a quasi-experimental analysis. Health Aff 2018; 37:591–599

22.

Haberman M, Pear R: Trump tells Congress to repeal and replace health care law “very quickly.” NY Times, Jan 10, 2017

23.

Drake C, Anderson DM: Terminating cost-sharing reduction subsidy payments: the impact of Marketplace zero-dollar premium plans on enrollment. Health Aff 2020; 39:41–49

24.

Eligibility for the Premium Tax Credit. Washington, DC, Internal Revenue Service, 2020. https://www.irs.gov/affordable-care-act/individuals-and-families/eligibility-for-the-premium-tax-credit. Accessed April 10, 2020

25.

Giovannelli J, Curran E: Factors affecting health insurance enrollment through the state marketplaces: observations on the ACA’s third open enrollment period. Issue Brief Commonw Fund) 2016; 19:1–12

26.

Stopka TJ, Hutcheson M, Donahue A: Access to healthcare insurance and healthcare services among syringe exchange program clients in Massachusetts: qualitative findings from health navigators with the iDU (“I do”) Care Collaborative. Harm Reduct J 2017; 14:26

27.

Pollitz K, Tolbert J, Diaz M: Data Note: Limited Navigator Funding for Federal Marketplace States. Menlo Park, CA, Kaiser Family Foundation, Nov 13, 2019. https://www.kff.org/private-insurance/issue-brief/data-note-further-reductions-in-navigator-funding-for-federal-marketplace-states/. Accessed July 5, 2020

28.

Zur J, Musumeci M, Garfield R: Medicaid’s Role in Financing Behavioral Health Services for Low-Income Individuals. Menlo Park, CA, Kaiser Family Foundation, June 2017. http://files.kff.org/attachment/Issue-Brief-Medicaids-Role-in-Financing-Behavioral-Health-Services-for-Low-Income-Individuals. Accessed July 6, 2020

29.

Abraham AJ, Rieckmann T, Andrews CM, et al: Health insurance enrollment and availability of medications for substance use disorders. Psychiatr Serv 2017; 68:41–47

30.

Lillie-Blanton M, Stone VE, Snow Jones A, et al: Association of race, substance abuse, and health insurance coverage with use of highly active antiretroviral therapy among HIV-infected women, 2005. Am J Public Health 2010; 100:1493–1499

31.

Venkataramani AS, Chatterjee P: Early Medicaid expansions and drug overdose mortality in the USA: a quasi-experimental analysis. J Gen Intern Med 2019; 34:23–25

32.

Snider JT, Duncan ME, Gore MR, et al: Association between state Medicaid eligibility thresholds and deaths due to substance use disorders. JAMA Netw Open 2019; 2:e193056

33.

Blavin F, Karpman M, Kenney GM, et al: Medicaid versus Marketplace coverage for near-poor adults: effects on out-of-pocket spending and coverage. Health Aff 2018; 37:299–307

34.

Gordon SH, Sommers BD, Wilson IB, et al: Risk factors for early disenrollment for Colorado’s Affordable Care Act Marketplace. Med Care 2019; 57:49–53

35.

McGuire TG, Newhouse JP, Normand S-L, et al: Assessing incentives for service-level selection in private health insurance exchanges. J Health Econ 2014; 35:47–63

36.

Wallace NT, McConnell KJ, Gallia CA, et al: Benefit policy and disenrollment of adult Medicaid beneficiaries from the Oregon health plan. J Health Care Poor Underserved 2010; 21:1382–1394

37.

Karpman M, Long SK, Bart L: The Affordable Care Act’s Marketplaces expanded insurance coverage for adults with chronic health conditions. Health Aff 2018; 37:600–606

38.

Glied S, Solis-Roman C: What Will Be the Impact of the Employer Mandate on the US Workforce? Issue Brief, pub 1778. New York, Commonwealth Fund, Oct 2014

39.

Olfson M, Wall M, Barry CL, et al: Effects of the Affordable Care Act on private insurance coverage and treatment of behavioral health conditions in young adults. Am J Public Health 2018; 108:1352–1354

40.

Capoccia VA, Grazier KL, Toal C, et al: Massachusetts’s experience suggests coverage alone is insufficient to increase addiction disorders treatment. Health Aff 2012; 31:1000–1008

41.

Mojtabai R, Olfson M, Sampson NA, et al: Barriers to mental health treatment: results from the National Comorbidity Survey Replication. Psychol Med 2011; 41:1751–1761

42.

Gertner AK, Robertson AG, Jones H, et al: The effect of Medicaid expansion on use of opioid agonist treatment and the role of provider capacity constraints. Health Serv Res 2020; 55:383–392

43.

Venkataramani AS, Bair EF, O’Brien RL, et al: Association between automotive assembly plant closures and opioid overdose mortality in the United States: a difference-in-differences analysis. JAMA Intern Med 2020; 180:254–262