Depression is a very common disorder, with a lifetime prevalence of nearly 17% in a recent large community sample (

1 ). With the advent of newer antidepressants, such as selective serotonin reuptake inhibitors (SSRIs), the pharmacologic treatment of depression has become more common but also more costly. In 2000, the last year in which all of the major SSRIs were available exclusively in their nongeneric form, domestic sales of antidepressants reached $10.4 billion (

2 )—expenditures that were greater than for any other category of medication. In fact, of the top ten drugs by retail sales in that year, three were antidepressants—fluoxetine, $2.6 billion; sertraline, $1.9 billion; and paroxetine, $1.8 billion.

There is no compelling evidence that any one SSRI antidepressant is clinically superior to another (

3,

4,

5 ). It has been suggested that in the context of selecting initial SSRI antidepressant treatment, all things being equal, the use of cost in determining the initial treatment in this category of medications is "prudent, ethical and reasonable"(

6 ).

In May 2002 a generic form of fluoxetine became available at Department of Veterans Affairs (VA) medical centers. As a result the average daily cost of fluoxetine treatment in the VA dropped from $1.47 to $.08—a cost decrease of 95%. In a system that spent nearly $180 million in the previous year on antidepressants, this price drop represented a potential opportunity for substantial cost savings.

This study was designed to determine whether availability of the first generic product in this relatively expensive class of medications was associated with an increase in its use compared with other medications.

Methods

This study was approved by the institutional review board of the VA Connecticut Healthcare System. Because of the nature of the study, individual informed consent was not obtained.

The sample included veterans whose records indicated that they received substantial outpatient mental health treatment and also initiated a new period of antidepressant pharmacotherapy in the VA in fiscal year (FY) 2001 and FY2003 (October 1 to September 30)—the year before and the year after generic fluoxetine became available.

Patient-specific data were obtained from the VA Patient Encounter and Patient Treatment Files. These files record diagnostic and provider data for each outpatient visit and basic data on all completed episodes of inpatient care provided at VA medical centers. Antidepressant medication records for FY2001 and FY2003 were obtained from the national Drug Benefit Management System and linked by using encrypted Social Security numbers.

The sample was operationally defined to include patients who had six or more outpatient encounters in a specialty mental health outpatient clinic or a hospitalization in a psychiatric inpatient unit in the year of interest and who had no record of an antidepressant prescription in the VA in the first four months of the fiscal year. A visit threshold was imposed in an attempt to ensure that patients were actually receiving treatment in the VA for psychiatric issues. Antidepressant prescriptions that were filled in the subsequent eight months of the fiscal year were considered "new antidepressant starts." Medications categorized as antidepressants with at least 100 new starts in FY2001 included amitriptyline, bupropion, citalopram, desipramine, doxepine, fluoxetine, fluvoxamine, imipramine, mirtazapine, nefazadone, nortriptyline, paroxetine, sertraline, trazodone, and venlafaxine.

Additional information about utilization of inpatient and outpatient psychiatric services during each year, age, gender, race or ethnicity, income, and psychiatric diagnoses was obtained from VA administrative databases.

Chi square statistics were used to compare the statistical significance of changes from FY2001 to FY2003 in the proportion of both new starts and price per day for each antidepressant.

Results

Altogether, 55,673 patients met the study entry criteria in FY2001 and 48,002 in FY2003. During these years the VA recorded at least one mental health visit for 704,340 and 781,459 patients, respectively. Although numerous significant differences were found between the groups in each fiscal year, which reflected the large sample, both groups included large proportions of patients with more than ten outpatient visits and with diagnoses of dysthymia, alcohol abuse or dependence, posttraumatic stress disorder and other anxiety disorders, and major depression. The two groups consisted primarily of patients coded as white, although those with missing racial or ethnic data accounted for the largest category in both years.

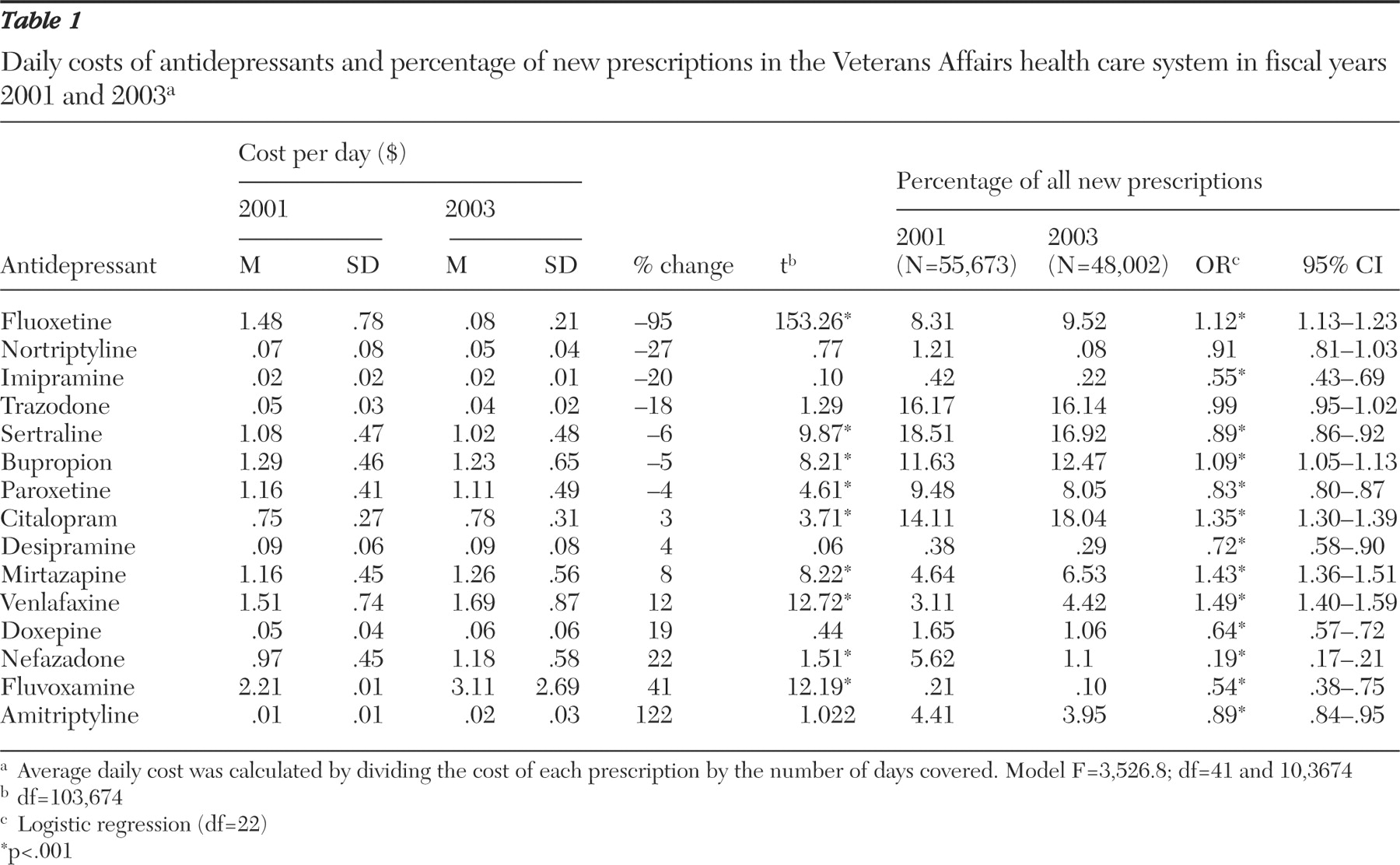

From FY2001 to FY2003 the percentage of new starts with fluoxetine (both branded and generic) increased by only 1.2%—from 8.3% to 9.5% (

χ 2 =46.79, df=1, p<.001). In terms of dollars spent for fluoxetine, new starts accounted for $1,002,000 in FY2001 and $33,281 in FY2003. Although fluoxetine was the only drug to become available in generic form, price changes, albeit smaller, were noted for several other drugs (

Table 1 ). Of the 15 antidepressants studied, only one (bupropion) showed the expected relationship between an increase in use (albeit less than 1%) and decreased cost. In fact, the other three antidepressants for which use increased (citalopram, mirtazapine, and venlafaxine) all had significant increases in cost. Finally, for two medications (paroxetine and sertraline) decreased use was associated with a decrease in cost. Logistic regression analyses, controlling for potentially confounding patient characteristics, yielded the same results.

Discussion and conclusions

The percentage of new prescriptions (both branded and generic) for the antidepressant fluoxetine significantly increased after its release as a generic drug at only 5% of its previous cost—but only from 8.3% to 9.5% of new antidepressant starts. In addition, during this same period, three antidepressants that were more expensive showed greater increases in new prescriptions.

It thus appears that in the VA nationally, there was no robust increase in the proportion of new fluoxetine prescriptions after its release as a low-cost generic. It is clear that the introduction of generic fluoxetine presented an opportunity for substantial cost savings, with the potential to decrease medication costs in this population of patients by approximately 90%. That is, if generic fluoxetine had been substituted in FY2003 for the top ten other antidepressants, prescription costs for this group of patients would have decreased from $3.2 million to $311,000. The lack of response is likely to reflect price insensitivity in a system in which neither the prescriber nor the patient is exposed to any direct financial repercussions from the price of prescribed medications.

Our data also reflect an absence of a systematic administrative effort to minimize medication costs among equivalent treatments. Although there are published examples of individual VA hospitals attempting to respond to differences in drug acquisition costs (

7 ), such efforts have not been coordinated at a national level. Moreover, a recent article has described some of the impediments to the use of cost-effectiveness considerations in formulary management in the VA, including resistance among physicians and other stakeholders (

8 ).

Several methodological limitations of this study deserve mention. First, the study examined only new starts of antidepressant prescriptions and did not address continued treatment. However, one would expect even less of a shift in continuing medications because both patient and prescriber are usually reluctant to change medications during treatment. Second, our definition of new antidepressant starts is based on administrative records, and their use for this purpose has not been validated. Third, some of the antidepressants may have been prescribed for indications not shared with fluoxetine—such as bupropion for smoking cessation—and one would not expect this use to be sensitive to the decreased cost of fluoxetine. Fourth, setting the threshold at six outpatient visits to a specialty mental health clinic or an inpatient hospitalization may have eliminated many patients who were treated in the primary care clinics in less than six visits. Thus, although most treatment for depression occurs in primary care clinics, our data are more reflective of treatment in the mental health clinics.

Finally, we do not know why prescribers chose the medications they did. They might have considered fluoxetine to be a less attractive antidepressant choice, concerned that it is less efficacious or more problematic, with a longer half-life and increased potential for drug-drug interactions. Similarly, because fluoxetine has been available for more than a decade, some of the patients for whom a new antidepressant start was contemplated may well have failed previous trials of fluoxetine and so were not considered candidates for retrial of this agent. Our methodology precludes addressing these very important issues, including to what extent impressions were shaped by published data versus marketing by pharmaceutical companies.

Our data suggest that there are untapped opportunities to realize savings in antidepressant use. Similar opportunities may arise with other classes of medications, such as second-generation antipsychotics, when generics become available. These savings will be realized only if administrative procedures are designed to take advantage of them and are not seen as unacceptably intrusive in terms of prescribers' and patients' autonomy.

Acknowledgments and disclosures

Dr. Sernyak has received honoraria from and is a consultant to Pfizer, Inc. Dr. Rosenheck has received research support from Eli Lilly and Company, Janssen Pharmaceutica, AstraZeneca, and Wyeth. He has been a consultant to GlaxoSmithKline, Bristol-Myers Squibb, and Janssen Pharmaceutica.