Since the enactment of the Affordable Care Act (ACA) in 2010 and its full implementation in 2014, the number of uninsured individuals in the United States has declined considerably (

1). The increase in insurance coverage is the result of various provisions of the ACA, such as the expansions in coverage through Medicaid, the health insurance exchanges, and the young adult mandate that allows individuals ages 19 to 25 to stay on their parents’ employer-sponsored insurance (

1). These ACA provisions are also contributing to improved access to primary care, improvements in self-reported health status, and affordability of care through lower out-of-pocket payments (

2,

3). Despite these gains, more than 29 million adults ages 18 to 64 still lacked health insurance coverage in 2014, according to the 2014 National Survey on Drug Use and Health (NSDUH) (

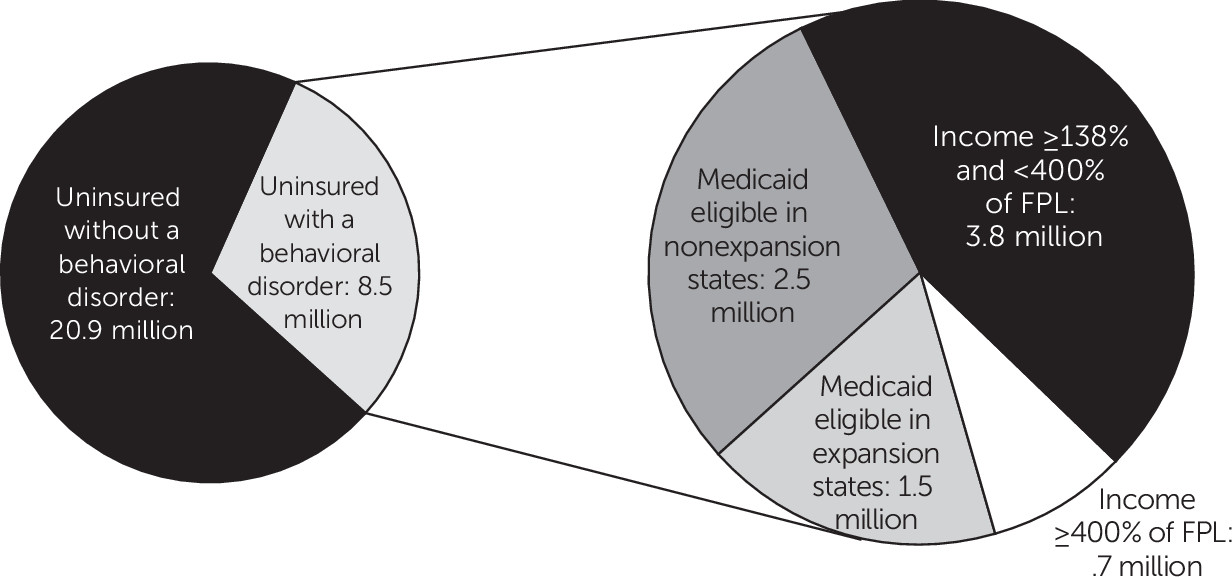

Figure 1).

Approximately 29% (8.5 million individuals) of the population remaining uninsured in 2014 had a behavioral health–related condition (that is, either a mental disorder or a substance use disorder).

Figure 1 shows that most of the uninsured individuals with a behavioral health condition (approximately 92%) were eligible for some form of assistance in gaining coverage under the ACA—for example, either they had incomes below 138% of the federal poverty level (FPL), which would make them eligible for Medicaid if they lived in an expansion state, or they had incomes between 138% and 399% of the FPL and were qualified for cost-sharing subsidies or tax credits through the health insurance exchanges. Of the four million uninsured individuals with a behavioral health condition who were Medicaid eligible in 2014, 2.5 million lived in a Medicaid nonexpansion state. Of the 4.5 million who were eligible to participate in the health insurance exchanges, 3.8 million were qualified for a subsidy or tax credit. Although several reports have examined the characteristics of the remaining uninsured population (

2,

4), little is known about uninsured individuals with a behavioral health condition.

Research has demonstrated that the uninsured are less likely than those with insurance to receive preventive care and services for major general medical conditions and chronic diseases and that having insurance can decrease the likelihood of experiencing depression and stress (

5). For individuals with behavioral health conditions, lack of insurance can be particularly problematic (

6). Using national data, recent studies have found that among persons with a mental illness or a substance use disorder or both, those with no health insurance were significantly less likely to receive treatment than those with any type of insurance (

7,

8). The literature also suggests that when individuals gain health insurance coverage, an eventual increase in use of behavioral health services is expected (

6). In addition, among uninsured adults with any mental illness, a significant proportion reported that they perceived an unmet need for mental health treatment; however, only a very small proportion of those with a substance use disorder reported a need for treatment for their disorder (

7,

8).

A number of previous studies have described the group of individuals who remain uninsured after ACA implementation. This study is the first to focus on the remaining uninsured individuals with behavioral disorders, a particularly vulnerable group. Using NSDUH data, this study examined the characteristics of adults with behavioral disorders who remained uninsured in 2014, the most recent year for which data were available, including their demographic characteristics, general medical status, and use of behavioral health services and the emergency department. Understanding the characteristics of these individuals will be helpful to states, federal agencies, and other stakeholders in developing and disseminating approaches to provide treatment and coverage.

Methods

This study utilized data from the 2014 NSDUH, a nationally representative survey of the noninstitutionalized U.S. population conducted annually by the Substance Abuse and Mental Health Services Administration. The NSDUH collects detailed information on use of alcohol and illicit drugs, mental and substance use disorders, and behavioral health treatment utilization.

Using

DSM-IV criteria specified during the year prior to the survey interview (

9), the NSDUH asks respondents questions to assess past-year symptoms of substance use disorders (substance dependence or abuse). It includes such symptoms as withdrawal, tolerance, use in dangerous situations, trouble with the law, and interference in major obligations at work, school, or home during the past year. The variable for substance use disorder in this study reflected whether the respondent had an alcohol use disorder or any illicit drug use disorder. Using

DSM-IV criteria specified during the year prior to the survey interview, the NSDUH also includes questions assessing any mental illness and serious mental illness during the past year. Any mental illness is the most comprehensive measure of mental illness available in the NSDUH and is defined as having symptoms of sufficient duration to meet

DSM-IV criteria for a mental or an emotional disorder (excluding developmental disorders and substance use disorders). Serious mental illness is defined as having a mental disorder that results in serious functional impairment that substantially interferes with or limits one or more major life activities. Because the ACA’s insurance expansions primarily affect the nonelderly population and because the focus of the study was on uninsured individuals with a behavioral disorder, the sample was restricted to those ages 18 through 64 with either a substance use disorder or any mental illness who did not have any health insurance coverage (unweighted N=2,300). All estimates were weighted to account for NSDUH’s complex survey design and to make the estimates nationally representative (weighted N of approximately 8.5 million).

In this study, uninsured individuals with behavioral disorders were categorized into four groups on the basis of their income and, in the case of low-income individuals (<138% of the FPL), whether their state had expanded Medicaid. Individuals with incomes <138% of the FPL were categorized as being eligible for health insurance coverage under the ACA’s Medicaid expansion provision. This group was further categorized into those living in a state participating in the Medicaid expansion and those living in a nonexpansion state. Respondents with incomes ≥138% of the FPL were grouped into two categories: those with incomes <400% of the FPL (those who would qualify for a federal subsidy through cost-sharing or a tax credit in the health insurance exchanges) and those with incomes ≥400% of the FPL (those who could participate in the exchanges but would not qualify for a subsidy). Descriptive statistics (weighted percentages, standard errors, and chi-square test statistics) for a wide range of variables are reported for these four groups.

In addition to examining demographic characteristics, such as age, gender, race-ethnicity, marital status, and education, this study looked at respondents’ use of any inpatient and outpatient behavioral health services and use of the emergency department. Any inpatient behavioral health treatment was defined as services received for mental health or substance abuse during the past 12 months at either a hospital or a mental health facility or a residential drug or alcohol rehabilitation facility that resulted in an overnight stay. Outpatient behavioral health treatment was defined as receiving services as an outpatient during the past 12 months at a hospital or a mental health facility or at a drug or alcohol rehabilitation facility. Outpatient behavioral health treatment also included services received for a mental or substance use disorder at a doctor’s office or other location that did not result in an overnight stay. An emergency department visit was defined as being seen in an emergency department at least once during the past 12 months. Other characteristics examined in the study included the respondents’ self-rated general medical status, suicidal behavior (ideation and attempt), criminal justice involvement (being arrested or booked or on probation or parole in the past 12 months), residence in a rural or urban area, employment status, and occupational category.

Results

Among the uninsured population with a behavioral health condition who would qualify for coverage under the Medicaid expansion, approximately 74% had any mental illness and 47% had a substance use disorder (

Table 1). The proportion with any mental illness and a co-occurring substance use disorder was 21%. Approximately 20% reported past-year suicidal ideation, and less than 3% reported a suicide attempt. Rates of suicidal behavior (ideation or attempt) did not differ significantly between respondents in Medicaid expansion and nonexpansion states. The rate of inpatient treatment also did not differ between respondents in Medicaid expansion and nonexpansion states. The rate of outpatient behavioral health treatment was higher among respondents in nonexpansion states compared with expansion states, but the difference was not statistically significant. The rate of emergency department visits was high; 46% of the Medicaid-eligible population with a behavioral health condition reported at least one emergency department visit during the past 12 months. The rate of emergency department visits was higher in nonexpansion states than in expansion states (48% versus 43%, p<.001). Less than half of respondents reported that their general medical condition was excellent or very good, and the difference between expansion and nonexpansion states was not statistically significant.

In terms of demographic characteristics, the largest portion of the uninsured Medicaid-eligible population was between the ages of 26 and 35 in both the expansion and nonexpansion states. Non-Hispanic white males constituted the largest race-ethnicity–gender group in expansion states, and non-Hispanic white females constituted the largest group in nonexpansion states. Among these low-income individuals with behavioral health conditions, 68% reported a high school education or less, 37% reported having a full-time job, 23% reported having a part-time job in the past 12 months, and approximately 18% had past-year criminal justice involvement. Most were employed in either blue-collar occupations (for example, construction, moving, and installation) or clerical and services occupations (for example, food services, sales, and office support). A large portion of the sample (84%) lived in an urban location, and 54% were never married.

Many characteristics of individuals with higher incomes (that is, those who would qualify for participation in the health insurance exchanges) were similar to those of the Medicaid-eligible population (

Table 2). Rates of any mental illness, serious mental illness, substance use disorder, any mental illness and a co-occurring substance use disorder, and suicidal behavior were very similar between the two groups.

Compared with the rate of emergency department use in the group that would be eligible for Medicaid expansion (46%), rates were lower in the group that would qualify for the health exchanges; those with incomes ≥400% of the FPL had the lowest rate (27%). In the exchange-eligible group, the largest age group was 26 to 35, and non-Hispanic white males constituted the largest race-gender group. Rates of having some college education or being a college graduate were higher in the exchange-eligible group compared with the Medicaid-eligible group. More than 50% of those who would qualify for the health exchanges reported having a full-time job; however, like the Medicaid-eligible group, most of them were employed either in blue-collar or clerical and services occupations.

Discussion and Conclusions

This study found that 29% of the remaining uninsured adults ages 18 to 64 had a behavioral disorder. More than 90% of adults who remained uninsured and who had a behavioral health disorder were eligible for some form of subsidy either through Medicaid (assuming that their state participates in Medicaid expansion) or the health insurance exchanges. However, more than 60% of the Medicaid-eligible individuals (2.5 million of four million) lived in a nonexpansion state. Among the exchange-eligible individuals, approximately 84% (3.8 million of 4.6 million) had incomes between 138% and 400% of the FPL. As expected, use of behavioral health treatment was very low in the population that remained uninsured; however, emergency department use was high, especially among those eligible for Medicaid.

Recent reports, which gained substantial media attention, documented a substantial increase between 1999 and 2013 in the all-cause mortality of middle-aged, non-Hispanic white men and women in the United States (

10). Since 1968, death rates declined by nearly 2% per year across most age groups and across racial and ethnic groups. However, between 1999 and 2014, mortality rates rose for white adults ages 22–56, peaking at around age 30 and age 50. The researchers concluded that three causes of death accounted for the increase in midlife mortality among white Americans: accidental poisonings (mostly drug overdoses), suicides, and chronic liver diseases and cirrhosis associated with alcohol consumption. These reports highlighted the importance of the results of this study, which found that the same demographic group represented the largest proportion of individuals with a behavioral disorder who remained uninsured. Approximately 47% of uninsured individuals with a behavioral health condition who were eligible for Medicaid had a substance use disorder, 20% had a serious mental illness, and 21% had any mental illness and a co-occurring substance use disorder.

These recent research reports also revealed a multifaceted phenomenon, in which mortality rates for middle-aged whites stopped declining—or actually increased—across a broad range of health conditions, including most of the leading causes of death for this group. For example, after rapidly declining between 1968 and 1998, mortality from heart disease essentially leveled off for this population between 1999 and 2014, whereas for blacks and Hispanics, heart disease death rates continued their rapid decline. This midlife mortality phenomenon has been noted to be especially severe in certain regions of the country (for example, in West Virginia, Mississippi, Oklahoma, Tennessee, Kentucky, Alabama, and Arkansas). This finding increases existing concerns over the continuing lack of health insurance among some groups, particularly because several of the states with the highest mortality trends did not expand their Medicaid program to cover all low-income adults (

11). Studies have also found that the mortality gap is concentrated among whites who lack a four-year college degree (

10,

11), a subpopulation that constitutes a substantial share of uninsured individuals with a behavioral health condition.

Although this is the first study to document the characteristics of the population with a behavioral health condition that remained uninsured in 2014, it had several limitations. The NSDUH question about insurance coverage pertains only to the time at which the survey is administered—that is, respondents indicate whether they are covered by any of the types of health insurance listed (private employer-sponsored insurance or insurance through public sources such as Medicaid or Medicare) or whether they do not have health insurance coverage. The survey provides a snapshot of coverage at a point in time but does not provide information on respondents’ previous health insurance status. This limitation is not unique to the NSDUH and is present in data from other surveys. In addition, the NSDUH includes retrospective questions about use of treatment. Specifically, respondents are asked about treatment obtained in the past 12 months. Particularly for interviews conducted in the early part of 2014, these questions captured information about experiences prior to the full enactment of the ACA. As a result, the measures of inpatient and outpatient treatment use and emergency department visits may have covered periods of 2013 before the ACA went fully into effect. However, limiting the analysis to individuals who were interviewed in the latter part of 2014, so that the past 12 months covered most of 2014, did not result in estimates for treatment and emergency department use that were different from those presented here. Furthermore, the NSDUH survey does not include questions regarding respondents’ attempts to gain health insurance coverage, nor does it explore reasons for not doing so. This information would be helpful in understanding why individuals with behavioral health conditions remained uninsured.

The Kaiser Survey of Low-Income Americans and the ACA, conducted in 2014, reported that among adults who were uninsured, 63% indicated that they did not attempt to gain coverage (

1). Because that was a survey of all uninsured adults, it is not clear whether lack of an attempt to gain coverage was the main reason for not having coverage among persons with behavioral health conditions. However, the literature indicates that individuals with behavioral disorders might benefit from outreach efforts to increase awareness and help the ACA reach its full potential of providing maximum coverage (

8). The large proportion of individuals with behavioral health conditions among the population remaining uninsured and the fact that a significant portion of this population would be eligible for either full or partial subsidies for health insurance coverage highlight the need for continued and focused public education efforts.

The findings of this study also highlight the need for developing new and innovative models for programs to encourage health literacy that could target individuals and groups who have not yet taken advantage of the opportunity to gain health insurance coverage (

12). For example, focusing outreach efforts to encourage enrollment on the health insurance exchanges among uninsured individuals who qualify for subsidies or among those who qualify for coverage under their parents’ insurance might help reduce the number of uninsured individuals. It would be important to explore their reasons for not doing so in order to understand the remaining barriers to coverage and to provide support that would encourage eligible individuals to take full advantage of what the ACA can provide. However, the relatively small number of behavioral health care providers (such as psychiatrists) who accept insurance may limit the ability of the ACA to reduce financial barriers and to expand access to care for those in need of behavioral health treatment (

13). A shortage of behavioral health providers participating in insurance networks can result in long wait times for an appointment or an inability to find a provider who accepts new patients. Thus efforts aimed at encouraging or incentivizing greater provider participation might also reduce barriers to treatment access. The detrimental impact on mortality of substance abuse and mental illness, coupled with low levels of education and economic opportunity in this population, underscore the urgency of addressing the issue of lack of health insurance coverage in all states.