The causes of rising medical liability insurance premiums nationwide are several and complex, but it appears that the most potent factor is the sharp increase in court awards, according to a report by the U.S. General Accounting Office (GAO).

The GAO’s review of the medical-malpractice marketplace nationwide and in seven specific states found multiple factors behind the steep increase in liability insurance that has caused some hospitals and physicians to cut back on services or—in rare cases—to halt services altogether.

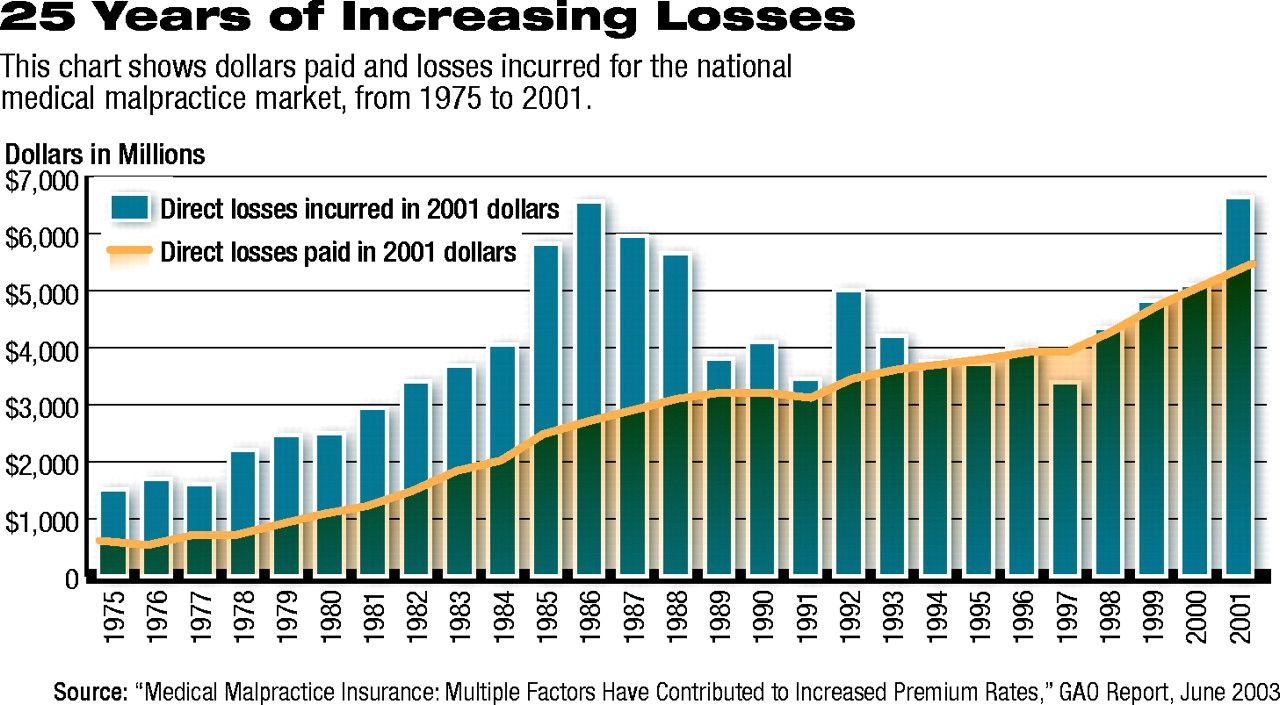

But the most prominent cause appears to be insurers’ losses on malpractice claims, the GAO said in its report, “Medical Malpractice Insurance: Multiple Factors Have Contributed to Increased Premium Rates.”

“Since 1998 insurers’ losses on medical-malpractice claims have increased rapidly in some states,” the report stated. “For example, in Mississippi the amount insurers paid annually on medical-malpractice claims, or paid losses, increased by approximately 142 percent from 1998 to 2001 after adjusting for inflation.

“We found that the increased losses appeared to be the greatest contributor to increased premium rates, but a lack of comprehensive data at the national and state levels on insurers’ medical-malpractice claims and the associated losses prevented us from fully analyzing the composition and causes of those losses,” the GAO stated.

Tort Reform More Needed Than Ever

The AMA cited the report as evidence of the need for tort reform and as a refutation of claims by opponents of reform—especially the trial lawyers association—who say the real reason for rising rates has to do with insurance company investment strategies. Those opponents say that insurance company premiums were artificially low during the bull-market years of the 1990s, when insurance companies were reaping profits from investments; now rates are rising to cover losses as investment income has decreased.

Not so, according to the AMA. “Today’s GAO report confirms what we have long held, that since 1999 medical liability premiums have skyrocketed in some states and specialties—and increasing awards are the main driver,” said AMA President Donald J. Palmisano, M.D. “Today’s report also puts to rest two other trial-lawyer smokescreens: that insurance company gouging and/or stock market losses have caused the medical liability crisis.”

Palmisano cited the GAO’s report stating that bonds make up 80 percent of insurers’ investments and that “no medical malpractice insurers experienced a net loss on their investment portfolios.”

And he drew attention to the report’s finding that insurer “profits are not increasing, indicating that insurers are not charging and profiting from excessively high premium rates.”

“The GAO report also notes that insurance regulators in most states have the authority to deny excessive premium rates,” Palmisano said.

“The medical liability crisis in this country cannot be ignored,” he continued. “The debate in the Senate is not over whether the medical liability system is in crisis—but rather how we will solve this crisis. Today’s GAO report points to the main culprit: increasing awards. The reasonable cap on noneconomic damages that has been working in California is clearly the answer to the crisis.”

Seven States Surveyed

The GAO sampled seven states—California, Florida, Minnesota, Mississippi, Nevada, Pennsylvania, and Texas—and compared state and national trends. Within each state, the GAO interviewed one or both of the two largest and currently active medical-malpractice insurers, the state insurance regulator, and the state association of trial attorneys.

To analyze the factors contributing to the premium rate increases in the sample states and nationally, the GAO reviewed data provided by medical practice insurers to state insurance regulators, the National Association of Insurance Commissioners (NAIC), and A.M. Best, a firm that rates insurance companies’ overall financial strength.

While the report emphasized the role of increasing malpractice awards, the GAO does indicate that investment strategies and a host of other factors can influence the liability market, and the report stated that much of the data necessary for a complete understanding of market trends are not available.

“This lack of data is due, in part, to the nature of NAIC’s and states’ regulatory reporting requirements for all lines of insurance, which focus primarily on the information needed to evaluate a company’s solvency,” the GAO stated. “Most insurance regulators do not collect the data that would allow analyses of the severity and frequency of medical-malpractice claims for individual insurer operations within specific states.”

In response to the report, Alan Levenson, M.D., president and CEO of Psychiatrists’ Purchasing Group, which sponsors the APA-endorsed Professional Liability Insurance Program (PLIP), said psychiatry has not been the focus of controversy around liability premiums and that the profession continues to have among the lowest premiums on average.

Still, he said, the profession is not exempt from what is happening in all of medicine. “Generally, psychiatrists’ premiums have not risen with the same speed of [those of] other specialties, but we are feeling the impact of increasing costs across the board,” he said. “That has led to two years of premium increases [in the APA-endorsed PLIP] after four years of no increases at all.”

Levenson said premiums in the PLIP increased an average of 30 percent in 2002 and 10 percent in 2003. Insurance carriers are dropping out of the market, he added, which also has made it difficult for physicians in all specialties to purchase any malpractice insurance in some states.

Levenson added that the APA-endorsed program remains the largest source of malpractice insurance for psychiatrists, with 7,000 participants.

The GAO report is posted on the Web at www.gao.gov/new.items/d03702.pdf. ▪

A number of factors contribute to increasing medical liability premiums, including insurance company investment losses. However, increases in malpractice awards are the leading cause.

If you have the appropriate software installed, you can download article citation data to the citation manager of your choice. Simply select your manager software from the list below and click Download.

For more information or tips please see 'Downloading to a citation manager' in the Help menu.

View Options

View options

Login options

Already a subscriber? Access your subscription through your login credentials or your institution for full access to this article.

PsychiatryOnline subscription options offer access to the DSM-5-TR® library, books, journals, CME, and patient resources. This all-in-one virtual library provides psychiatrists and mental health professionals with key resources for diagnosis, treatment, research, and professional development.

Need more help? PsychiatryOnline Customer Service may be reached by emailing [email protected] or by calling 800-368-5777 (in the U.S.) or 703-907-7322 (outside the U.S.).

If the address matches an existing account you will receive an email with instructions to retrieve your username

Create a new account

Change Password

Password Changed Successfully

Your password has been changed

Login

Reset password

Can't sign in? Forgot your password?

Enter your email address below and we will send you the reset instructions

If the address matches an existing account you will receive an email with instructions to reset your password.

Change Password

Congrats!

Your Phone has been verified

×

As described within the American Psychiatric Association (APA)'s Privacy Policy and Terms of Use, this website utilizes cookies, including for the purpose of offering an optimal online experience and services tailored to your preferences. Please read the entire Privacy Policy and Terms of Use. By closing this message, browsing this website, continuing the navigation, or otherwise continuing to use the APA's websites, you confirm that you understand and accept the terms of the Privacy Policy and Terms of Use, including the utilization of cookies.